ESRS 2 – General disclosures

General basis for preparation of sustainability statements (BP-1)

Basis of reporting and framework conditions

This Sustainability Report has been prepared in reference with the Global Reporting Initiative (GRI) and is based on the requirements set out in the European Sustainability Reporting Standards (ESRS, Draft from July 31, 2025). All of the disclosures in the Sustainability Report are either based on the results of our double materiality analysis (DMA) or must be mandatorily disclosed in accordance with statutory requirements.

Consolidation scope and reporting period

The Sustainability Report has been prepared on a consolidated basis and comprises the relevant data for the financial year from January 1 to December 31, 2025. The consolidation scope of the Sustainability Report is generally consistent with the consolidated financial statements in accordance with Swiss GAAP FER and comprises all of the companies controlled by SFS. Any deviations from this are disclosed in the respective accounting principles. The consolidated financial statements have been prepared in accordance with Art. 48i and are applicable. An overview of the companies included can be found in the Financial Report 2025.

Statement

The SFS Group has taken into consideration the general requirements of ESRS 1 in the preparation of its sustainability statement and, in doing so, has applied the following provisions in accordance with ESRS 2 section 5:

- Application of significant discretionary decisions and information subject to considerable uncertainty (ESRS 1 section 86)

- Application of easements if the company discloses metrics that are not complete (ESRS 1 section 91)

- Changes in the preparation or presentation of sustainability information (ESRS 1 section 95)

- Reporting of errors in prior periods (ESRS 1 sections 96 and 97)

- Presentation of additional information (ESRS 1 sections 108 and 109)

- Use of easements for metrics in the value chain (ESRS 1 section 92)

Specific information in relation to phasing-in options (BP-2)

Time horizons

The time horizons used in this report are consistent with the definitions set out in ESRS 1:

- Short term: within the reporting year (in correspondence with the annual financial statements)

- Medium term: from the end of the short-term time horizon to a maximum of five years

- Long term: more than five years

Accounting policies

The accounting policies described in the report have been applied consistently for the reporting year and for comparison figures, where relevant.

The climate-related disclosures in accordance with TCFD are provided in the form of a PDF document in the reporting year and can be found in chapter ESRS E1).

Method for calculating greenhouse gas emissions

Environmental data for 117 locations was collected in the reporting year. The locations not included cause less than 3% of the total greenhouse gas emissions. The period under review is equivalent to the calendar year, with the data for December being estimated.

Greenhouse gases (Scope 1, 2 and 3) are calculated in accordance with the GHG Protocol (Corporate Accounting and Reporting Standard). The Global Warming Potential (GWP) factors used are based on the sixth IPCC Assessment Report (AR6). The emissions were calculated with the help of the REGIS expert system using secondary data from ecoinvent database version 3.12.

Scope 1

Scope 1 emissions include direct emissions from burning fossil fuels (including natural gas, heating oil, propane and methanol), using privately owned vehicles and operating materials (e.g. refrigerant losses).

Scope 2

Scope 2 emissions from electricity and district heating were calculated based on the market. In doing so, certificates of origin (Energy Attribute Certificates), contractually agreed energy mixes and – if no certificates existed – country-specific residual or market mixes were taken into consideration. In addition, location-based Scope 2 emissions were calculated.

Scope 3

Scope 3 emissions were calculated for all of the relevant categories based on secondary data (ecoinvent, average data method):

- Category 1: Purchased goods and services (raw materials, trading goods, packaging); outsourced services were not taken into consideration due to their immateriality

- Category 2: Capital goods based on annual expenditure, allocated to defined activity baskets taking regional factors into consideration

- Category 3: Fuel and energy-related activities based on Scope 1 and Scope 2 data

- Categories 4 & 9: Upstream and downstream transport and distribution, calculated on the basis of weight, distance and means of transport; extrapolations were used in instances of gaps in the data

- Category 5: Waste generated in operations, based on the type of waste, volume of waste and disposal procedure

- Category 6: Business travel, based on the distance and means of transport

- Category 7: Employee commuting, extrapolated based on random samples and the number of FTEs

- Category 8: Upstream leased assets (already included in Scope 1 and 2)

- Category 10: Processing of sold products (not material)

- Category 11: Use of sold products; emissions are model-based and rounded due to uncertainties

- Category 12: End-of-life treatment of sold products, based on the material composition, weight and disposal methods; emissions are rounded

- Category 13: Downstream leased assets (not material)

- Category 14: Franchises (not applicable)

- Category 15: Investments; pro rata emissions of the Sunil SFS Automotive Parts Co., Ltd. joint venture

- Other Scope 3 emissions: Road infrastructure, included in the secondary data used

Estimates, assessments and uncertainties

Where primary data was unavailable, secondary data, estimates and extrapolations were used, especially for greenhouse gas emissions and for locations for which environmental data was not able to be collected in full. The underlying assumptions are disclosed in the relevant sections.

Estimates are based on industry benchmarks, emissions factors and conservative assumptions. The resulting uncertainties arise in particular from the limited availability of data from upstream suppliers. The data quality is continuously being improved.

External assurance

The following metrics have been externally validated by Ernst & Young within the framework of the sustainability reporting:

- Scope 1, 2 and 3 greenhouse gas emissions

- Energy consumption

- Accident rate

- Further data on the workforce

These are marked accordingly in the respective tables with “limited assurance 2025.”

The Financial Report and the Compensation Report were audited by PricewaterhouseCoopers AG as statutory auditor.

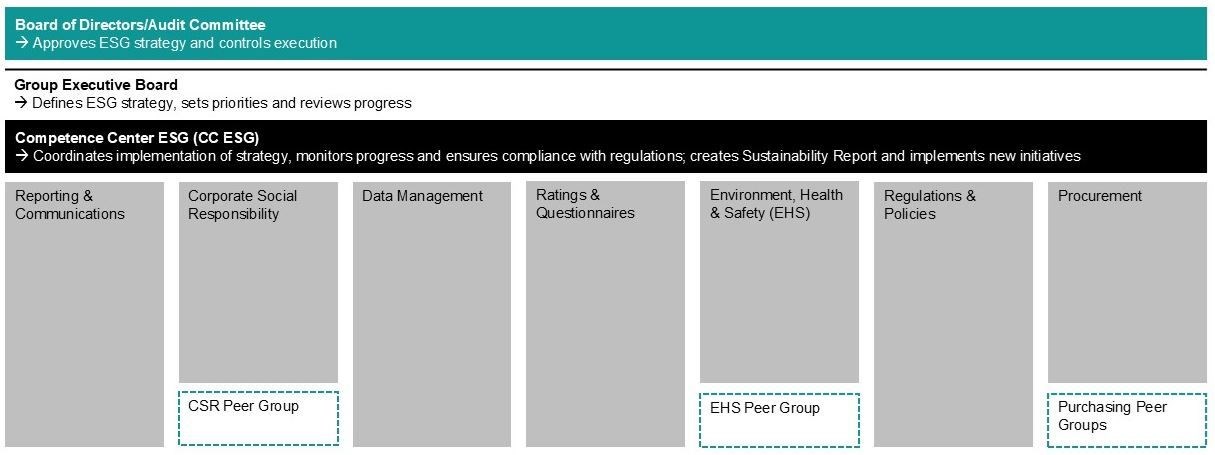

The role of the administrative, management and supervisory bodies in relation to sustainability (GOV-1)

Clearly defined governance structure

Responsibility for ESG topics is clearly defined within the SFS Group and enshrined at every level:

Board of Directors and Audit Committee

- 75% independent members, 25% women

- Approve the sustainability strategy and the Sustainability Report

- Monitor compliance with statutory requirements and the quality of reporting

- Incorporate material ESG aspects into strategic decisions and group-wide risk management (especially for investments, M&A activities and regulatory developments)

Group Executive Board (GEB)

- Is responsible for the content of the strategy

- Sets priorities, makes strategic decisions and reviews results and findings

- Sets and monitors ESG targets under the supervision of the Board of Directors

Competence Center ESG (CC ESG)

- Coordinates the group-wide implementation of the ESG strategy

- Monitors progress, initiates projects and ensures regulatory compliance

- Prepares the annual Sustainability Report

- Guarantees data quality, consistency and plausibility using the ESG reporting

- Organized into specialist areas such as Reporting & Communications, Corporate Social Responsibility, Data Management, Ratings, Environment Health & Safety, Regulations & Policies and Procurement

- Promotes group-wide exchanges and the further development of ESG-relevant topics via Peer Groups

This governance structure ensures that ESG topics are enshrined in strategy, implemented in operations efficiently and continuously adapted to new opportunities, risks and impacts (see also graphic below).

Material IROs in the reporting period

The following material sustainability topics and IROs were dealt with by administrative, management and supervisory bodies in the reporting year 2025:

- Climate change and CO₂ reduction (Scope 1–3)

- Energy consumption and efficiency

- Sustainable solutions and the circular economy

- Pollution in the value chain

- Training and education

- Diversity, equality and inclusion

- Supply chain due diligence and human rights risks

- Business ethics, integrity and compliance

- Occupational health and safety

A detailed overview of the priority ESG topics and IROs can be found in this chapter under “Interaction between material financial impacts, risks, and opportunities with strategy and business model (SBM-3)” ff. and “Material impacts, risks, and opportunities as well as disclosure requirements in the sustainability statement (IRO-2)” and in the Management Report.

Further information on qualifications and ESG expertise (GOV-1 und GOV-2)

Information on the members of the Board of Directors and the Group Executive Board, including resumes, qualifications and ESG-relevant expertise, can be found in section “Board of Directors” ff. of the Corporate Governance Report and in the GRI ESRS Interoperability Index (see GRI 2-9, 2-10, 2-11, 2-12, 2-13, 2-14, 2-16, 2-17, 2-18, and 2-26).

Inclusion of sustainability-related performance in incentive systems (GOV-2)

Group of people | Type of compensation | Sustainability-related performance criteria | Weighting | Definition and assessment |

Group Executive Board | Variable cash compensation, variable share-based compensation | CO2 reduction, renewable energies, occupational health and safety, equal treatment, training and education | Approx. 5% of variable cash compensation | Defined by the Board of Directors or the CEO, annual review and assessment by the Board of Directors |

Board of Directors | Fixed basic fee, committee compensation, fixed number of SFS shares | No sustainability-related performance criteria included in the compensation | – | Compensation is defined annually by the Board of Directors and approved by the Annual General Meeting |

Further details on the integration of sustainability-related performance in incentive schemes can be found in the Compensation Report.

Statement on due diligence (GOV-3)

The SFS Group has implemented a process for fulfilling its obligation to carry out due diligence as regards human rights and environmental issues in accordance with the OECD Guidelines for Multinational Enterprises and the principles of the UN Global Compact. This process extends to both its own business operations and the entire value chain.

The obligations to carry out due diligence as regards human rights and environmental issues are integrated into the SFS business processes. This includes the following components:

- The regular performance of supplier assessments in relation to social and environmental criteria

- A group-wide mandatory Code of Conduct and a Supplier Code of Conduct

- A systematic ESG risk analysis, which assesses the likelihood of occurrence and loss amount of risks

- Compliance audits at selected locations

- A comprehensive compliance system including anonymous reporting channels and a whistleblowing system for internal and external stakeholders

The effectiveness of environmental measures is monitored using defined key figures and target values. Deviations are analyzed and, if necessary, lead to adjustments to the measures. Both the implementation and the effectiveness of the measures are reviewed regularly.

With the aim of identifying, assessing and managing material risks and impacts, risk analyses are carried out, compliance reports are evaluated and measures are derived on an annual basis. External stakeholders are also regularly involved in this process, such as within the DMA, in dialogs with customers, suppliers and investors, as well as in targeted informational and participatory events.

SFS is expressly committed to respecting human rights and disapproves of all forms of child or forced labor. Compliance with these principles is a mandatory component of business operations and is set out in our sustainability guidelines and our Code of Conduct; it is also a prerequisite for working together with business partners. (see also ESRS G1).

Risk management and internal controls over sustainability reporting (GOV-4)

To ensure the quality and reliability of sustainability reporting, the SFS Group has established an internal management and control system for ESG-relevant information. Responsibility for sustainability reporting lies with the CC ESG, which manages the collection, consolidation and verification of the ESG data centrally.

In order to ensure completeness and consistency, all of the relevant metrics and qualitative information are validated. This includes a review by the specialist departments and the CC ESG as well as approval by the Group Executive Board and subsequently by the Board of Directors. The internal control system is reviewed on an annual basis and adapted where necessary. In addition, an external auditor is mandated for defined metrics. The governance and monitoring processes for controlling the ESG report data and for ensuring compliance with the ESRS requirements are components of the annual ESG report to the Board of Directors.

Strategy, business model and value chain (SBM-1)

Value chain

The SFS Group value chain comprises:

- Upstream levels: raw materials suppliers, materials and components suppliers, and logistics and IT service providers

- Internal level: Development, Production, Assembly, Quality Management, Distribution and Logistics

- Downstream levels: customers from the automotive, electronics, medical devices and construction industries as well as industrial manufacturing and end customers via the indirect distribution channel

All SFS activities are classified as sectors with high climate impact within the meaning of the ESRS and are covered by the following NACE codes: C25.11, C25.94, C29.32, C32.50, G46.62, G46.64.

The SFS Group strives to consistently respect environmental and social standards along the entire value chain and fulfill its due diligence obligation by means of suitable instruments (e.g. supplier audits and the rollout of the Supplier Code of Conduct).

Sustainability in the corporate strategy

Sustainability is firmly enshrined in the corporate principles and the Code of Conduct as part of our DNA and is a strategic driver within our value engineering approach. SFS uses an integrated approach to create innovative, resource-efficient and socially responsible solutions for customers and partners.

Interaction between sustainability and the strategy and business model

The ESG-relevant aspects have a considerable influence on the development of new products, the selection of suppliers, production operations and leadership. This takes into account the impact on environmental and climate issues, social and employee issues, respect for human rights, and aspects of responsible corporate governance. Scorecards are used to systematically evaluate product development in respect of environmental and social criteria. Furthermore, the strategic focus on low-emission processes, the circular economy and digitalization have an impact on efficiency gains along the entire value chain.

Changes in the strategy and business model

The following material changes were made in the reporting year 2025:

- Expansion of the sustainability goals to include new target values for CO₂ reduction in accordance with the SBTi

- Expansion of the targets in relation to the transparent value chain (further information on this topic is provided in section ESRS S2)

- Expansion of the training offering by means of a new e-learning platform

- Greater emphasis placed on ESG criteria in the product development process by means of mandatory scorecards for new products

Compare also strategy.

Interests and views of stakeholders (SBM-2)

The SFS Group engages in a continuous and structured dialog with a variety of internal and external stakeholders. The aim is to systematically establish and evaluate their expectations and views on key sustainability topics and incorporate these into corporate decision-making and management processes.

Main stakeholders and their expectations

The main stakeholders for us have been identified as part of a stakeholder analysis and comprise the following:

Stakeholder group | Expectations/interests | Dialog formats | Influence on SFS | Influence of SFS |

Employees | Working conditions, compensation, development, security, participation | Employee surveys, team events, CSR initiatives, intranet | Innovative capacity, productivity, employer attractiveness | Work and life quality, career prospects |

Management | Target achievement, efficiency, employee satisfaction, innovation | Management meetings, strategy workshops, further training | Strategy implementation, management of ESG topics | Framework conditions, resources, ESG requirements |

Shareholders and investors | Increase in value, ESG transparency, risk management, dividends | Annual General Meeting, investor meetings, roadshows, reports | Capital, strategic focus, governance | Shareholder value, dividends, ESG performance |

Customers | Quality, reliability, sustainability, innovation | Customer meetings, trade shows, feedback systems | Market success, innovation, reputation | Product quality, service, sustainable solutions |

Suppliers and supply chain employees | Partnership, fair conditions, plannable orders, sustainability | Supplier audits, IntegrityNext questionnaires, dialog formats | Quality, innovative capacity, supply security | Collaborations, ethical standards, sales volumes |

Authorities and regulatory bodies | Legal certainty as well as environmental, work and tax conformity | Meetings with authorities, reports, events | Regulatory requirements, market access | Tax revenue, jobs, compliance |

Society, municipalities, NGOs | CSR, environmental protection, local engagement | Events, fundraising campaigns, sponsorship, dialog formats | Acceptance, reputation, location quality | Public welfare, education, regional projects |

Media | Transparent information | Interviews, media conferences, media releases | Public perception, image | Access to information, positioning |

Universities and educational institutions | Cooperations, practical projects, promotion of young talent | MINT projects, presentations, dual study program, facility visits | Innovation, young skilled staff | Educational offerings, practical relevance, career opportunities |

Industry and sustainability associations | Industry networks, standards, sustainability initiatives | Association work, meetings, working groups, industry events | Industry standards, political framework conditions | Exchange of experiences, standardization, industry reputation |

Nature/environment | Conservation of resources, climate protection, biodiversity | Environmental reports, environmental management systems, sustainability projects | Raw material availability, local conditions, risks | CO₂ emissions, biodiversity contribution, protection of resources |

Focus on key external ratings

In 2025, SFS was assessed within the scope of the following external ratings or participated in the following assessments:

Rating/questionnaire | 2025 rating | 2024 rating | 2023 rating | Scale |

CDP (climate questionnaire) | B | B | B | A to F |

EcoVadis (ESG questionnaire) | In assessment | Bronze (64/100) | Silver (63/100) | Platinum to Bronze |

Ethos | B+ (51/100) | B+ (47/100) | A- (51/100) | A+ to C- |

Inrate, zRating | 66/100 | 66/100 | 69/100 | 100 to 0 |

ISS | C | C- | D+ | A+ to D- |

MSCI | A | A | AA | AAA to CCC |

Supplier Assurance (SAQ 5.0) | In assessment | B88 (location in Heerbrugg, CH) | B86 (location in Heerbrugg, CH) | A to D, 100 to 0 |

Sustainalytics | ESG risk status: high, 33.1 | ESG risk status: high, 30.2 | ESG risk status: medium, 26.3 | Negligible to severe |

UN Global Compact | Active | Active | Active | Active – inactive – not reporting |

Dialog and inclusion formats

The SFS Group maintains a wide range of communication and dialog formats, including:

- Employee surveys, employee meetings, training sessions and CSR initiatives (such as the Social Days)

- Management meetings, workshops and further training

- Annual General Meetings, investor meetings and roadshows

- Customer and supplier meetings, trade shows and feedback systems

- Cooperations with universities and educational institutions

- Regular media discussions and releases

- Involvement in associations, interest groups and industry initiatives

Consideration of stakeholder interests in strategy and management

The outcomes of stakeholder dialogs are systematically incorporated into the corporate strategy and sustainability management:

- Double materiality analysis with the involvement of all of the relevant stakeholder groups

- ESG reporting to administrative, management and supervisory bodies as well as to the CC ESG

- ESG communication via reports, dialog formats and digital channels

- Integration of stakeholder expectations in product development, the value chain and HR strategy

Changes to and impacts on stakeholder relationships

By enshrining ambitious ESG targets (including CO₂ reduction, employee development and health protection) in the Group’s strategy and signing up to the SBTi, strategic decisions were made that influence existing stakeholder relationships:

- Customers: improving customer loyalty through products with long-term added value

- Employees: increasing motivation and loyalty through attractive working conditions

- Investors: maintaining existing business relationships and gaining new responsible investors through increased transparency

- Society and the environment: improving the Group’s reputation and level of acceptance through active environmental and social projects

Flows of information to administrative, management and supervisory bodies (SBM-2, Abs. 43 a–c)

With the aim of regularly taking the interests of stakeholders into account, the following communication and reporting channels have been established:

- Stakeholder surveys and feedback evaluations with reports submitted to the Board of Directors and the Group Executive Board

- Quarterly ESG reports and annual sustainability reports for the Group Executive Board and the Board of Directors

- Direct dialog between the Group Executive Board, the CC ESG and stakeholders

- The CC ESG, which reports regularly to the Group Executive Board and reviews new regulatory requirements

Material financial impacts, risks and opportunities and their interaction with strategy and business model (SBM-3)

The SFS Group regularly analyzes and assesses the material impacts of its business operations on the environment, society and the economy, as well as the resulting risks and opportunities (IROs). These are systematically aligned with the corporate strategy and the business model, forming the basis for taking new strategic directions and making investment decisions.

Identification of the material IROs

As part of the double materiality analysis carried out in 2024, the main IROs were identified, taking into consideration stakeholder perspectives, regulatory requirements and the Group’s strategic targets.

Environmental topics: Climate change and energy efficiency

Impacts: global warming and the CO₂ footprint along the value chain

Risks: increased energy costs, supply uncertainties and physical asset risks due to natural disasters

Opportunities: cost savings due to energy efficiency, a competitive advantage due to low-CO₂ products and processes, and positive positioning due to SBTi targets

Planned steps to be taken:

- Implementation of the SBTi-compliant climate strategy (short-term and long-term target by 2030 respectively 2050)

Environmental topics: Air and soil pollution

Impacts: negative impact on the environment and health due to emissions (e.g. particulate matter, VOCs and NOx) and damage to the local air quality in production regions

Risks: stricter legal emissions limits and regulatory costs, as well as reputational risks due to negative impacts on residents and the environment

Opportunities: efficiency gains through low-emission technologies and processes, competitive advantages due to more environmentally friendly production and certifications, as well as improved relationships with stakeholders (authorities, municipalities and customers)

Planned steps to be taken:

- Reduction of volatile organic compounds (VOCs) through process optimizations

- R&D into the use of low-emission technologies and filtration systems

- Establishment of a group-wide monitoring system for air emissions

Environmental topics: Circular economy and conservation of resources

Impacts: consumption of resources and waste generated along the entire value chain

Risks: costs due to the inefficient use of resources, compliance violations and reputational damage

Opportunities: increase in competitiveness due to sustainable product designs and recycling solutions

Planned steps to be taken:

- Promotion of product and process optimizations as regards material efficiency and recyclability

- Development of modular and reusable products in selected areas

Social topics: Occupational health and safety of our own workforce

Impacts: employee wellbeing and the reduction of occupational accidents

Risks: production outages, reputational damage and costs caused by lost working days

Opportunities: productivity gains, improved employer reputation and increased employee retention

Planned steps to be taken:

- No occupational accidents by 2030

Social topics: Training and dual education of our own workforce

Impacts: retention of skilled workers and innovative capacity

Risks: a lack of skilled workers and a reduction in competitiveness

Opportunities: positioning as an attractive employer and greater innovative capacity

Planned steps to be taken:

- Permanently 5–7% of employees worldwide to be enrolled in dual education and training programs

- Permanently fill 70% of management positions with internal candidates

Social topics: Diversity of our own workforce

Impacts: contribution to equal opportunities and social justice, as well as an improvement of innovative capacity through different perspectives

Risks: loss of competitiveness due to homogeneous teams, reputational damage in the case of a lack of diversity and inclusion, and difficulties in attracting employees in a global environment

Opportunities: increased attractiveness as an employer through a diverse and inclusive culture, better decision-making processes due to diverse teams and an increase in resilience to societal changes

Planned steps to be taken:

- Increase of the percentage of women in management roles and on the Board of Directors

- Systematic monitoring of diversity metrics

Social topics: Occupational health and safety and the prevention of forced and child labor of workers in the value chain

Impacts: influence on working conditions and human rights at suppliers and a contribution to health protection and a safe working environment

Risks: reputational damage due to human rights violations or breaches of labor law; disruptions in the supply chain due to social conflicts or misunderstandings, and liability risks on the grounds of international due diligence obligations

Opportunities: improvement of resilience and stability in the supply chain as well as the establishment and retention of long-term trusting relationships with suppliers

Planned steps to be taken:

- Continuation of the implementation of the Supplier Code of Conduct

- Performance of risk analyses and audits along the supply chain

- Establishment of training and support programs for suppliers

Governance topics: Responsible business conduct

Impacts: company reputation, compliance and stakeholder trust

Risks: damage to the Group’s image and financial loss due to non-compliance and ethical violations

Opportunities: improvement of employer and capital market attractiveness as well as resilience

Planned steps to be taken:

- Compliance training courses and internal audits

- Expansion of the compliance management system

Link to strategy and the business model

The identified IROs are closely linked to the business model and the strategic focus of the SFS Group. Sustainability is an integral part of the value engineering approach and shapes product development, internal processes and supply chain management. The ambitious targets in the areas of emissions reduction, the efficient use of raw materials, occupational safety and further training form the basis for a sustainable and future-proof corporate strategy, safeguard competitiveness and increase resilience to external ESG risks.

Consideration in management and decision-making processes

The results of the IRO assessment are communicated to the Board of Directors and Group Executive Board on an annual basis. The CC ESG, which is active across the Group, ensures that measures are derived and implemented and the achievement of targets is systematically tracked. The IRO analysis is an integral part of the annual strategy review and investment planning.

Description of the process to identify and assess material impacts, risks and opportunities to be reported on (IRO-1)

In accordance with the CSRD and ESRS requirements, we have implemented a systematic process to identify and assess the material impacts, risks and opportunities (IROs). This process adheres to the principle of double materiality and takes into consideration both the impacts of our company on the environment and society (impact materiality) as well as the impacts of external sustainability topics on our business operations, financial situation and performance (financial materiality).

The double materiality analysis (DMA) encompasses all of the relevant locations and business activities of SFS Group AG and includes both internal and value chain-related impacts and risks.

The results of this process form the basis for the content of this report as well as for the further development of our sustainability strategy and the targets we set ourselves.

- Business model analysis

Understanding of the different business models of our segments, the value chain, the end markets (that are primarily located in Asia, Europe and North America), products and services in an ESG context - Topic identification (long list)

A collection of potentially relevant topics based on IROs, standards and internal analyses - Topic assessment and limitation (medium list)

Preselection of relevant topics by means of an internal assessment in accordance with defined IRO criteria - Stakeholder survey

An online survey of internal and external stakeholders on impact and financial materiality - Internal workshops

Discussion and refinement of the survey results, prioritization, and the finalization of the short list of material IROs - Utilization of the results

Integration of the results into the report, management and the sustainability strategy

Responsibilities and assessment logic

The double materiality analysis was coordinated by the CC ESG in close cooperation with the Group Executive Board. The identified impacts were assessed based on defined criteria in accordance with the ESRS, taking into account the scale, scope, likelihood and – in the case of negative impacts – irremediability.

The materiality of risks and opportunities was assessed on the basis of likelihood and the potential financial scale. A qualitative scale of 1 (low scale) to 5 (high scale) was used for this. In addition, qualitative criteria were taken into consideration to ensure the consistency of the group-wide assessment.

The results of the DMA were approved by our senior decision-makers, the Board of Directors and our Group Executive Board, and were then shared with all workshop participants.

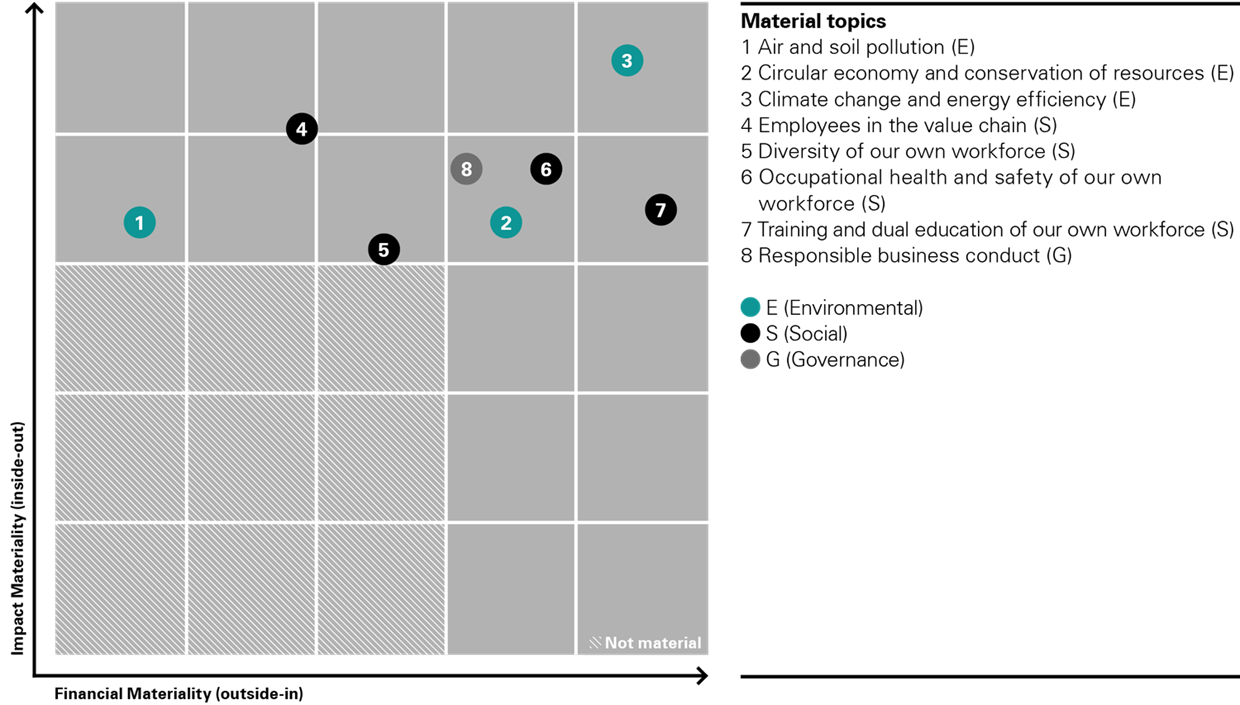

Materiality matrix

Material impacts, risks and opportunities as well as disclosure requirements in the sustainability statement (IRO-2)

Topic | Material impacts | Risks | Opportunities | Planned measures and time frame |

Climate change and energy efficiency | Carbon footprint of SFS and the value chain | Natural hazards, supply bottlenecks, energy cost increases | Competitive advantage due to low-CO₂ products and processes, cost savings | Implementation of the SBTi-compliant climate strategy (“short-term target” and “long-term target” by 2030 and 2050, respectively) |

Soil contamination and air pollution | Negative impact on the environment and health due to emissions, damage to the local air quality in production regions | Regulatory costs, reputational risks | Efficiency gains through low-emission technologies and processes, competitive advantages due to more environmentally friendly production | R&D into the use of low-emission technologies and filtration systems, establishment of a group-wide monitoring system for air emissions |

Circular economy | Consumption of resources and waste along the entire value chain | Compliance risks, costs due to inefficient use of resources | Competitive advantage due to recyclable and resource-efficient products | Product/process optimizations, development of modular products from 2025 |

Occupational health and safety | Health, safety and wellbeing of employees | Production outages, costs caused by lost working days, reputational damage | Productivity, employer attractiveness, increased loyalty | Halving the accident rate by 2025, long-term “zero accidents” target by 2030 |

Training and education | Development of skilled workers and innovative capacity | A lack of skilled workers, Group’s competitiveness compromised | Employer attractiveness, innovative capacity, higher employee retention | 5–7% of employees enrolled in dual programs, 70% of management positions filled internally |

Responsible conduct (governance) | Company reputation, compliance, stakeholder trust | Damage to the Group’s image and financial loss due to ethical violations | Improvement of employer and investor attractiveness, resilience | ESG training courses, expansion of compliance management from 2025 |

Diversity | Creativity, innovative capacity, employer image | Unilateral corporate culture, reputational risks | Better quality of decision-making, broader innovation basis | Expansion of DEI programs, KPIs for managers from 2025 |

Supply chain (labor laws and human rights) | Working conditions, environmental and social standards in the supply chain | Reputational and supply shortage risks, legal sanctions | Reputation boost, stable and resilient supply chains | Binding Supplier Code of Conduct, IntegrityNext audits |